For anyone who has navigated the often congested lanes of I-285 or endured a downpour on the Downtown Connector, it is no surprise that car insurance premiums in Atlanta can be higher than in other parts of Georgia. The city’s unique challenges, from dense traffic to complex accident claims, often contribute to rates that are higher than the statewide average.

This report demonstrates that a generic “average” rate may not reflect an individual’s actual premium. The true path to savings involves three core steps. First, understanding the specific personal and demographic factors that influence a rate is crucial. Second, identifying and leveraging available discounts can lead to potential savings. Third, and importantly, an individual must engage in a thorough comparison of quotes from multiple providers, as a company that is affordable for one driver profile may not be for another. This guide provides the data and a clear, actionable roadmap to navigate this complex market and find the suitable coverage.

Section 1: The Atlanta Factor: Why Your Premiums Are Higher

1.1. The Price of the Perimeter: Atlanta vs. Georgia Rates

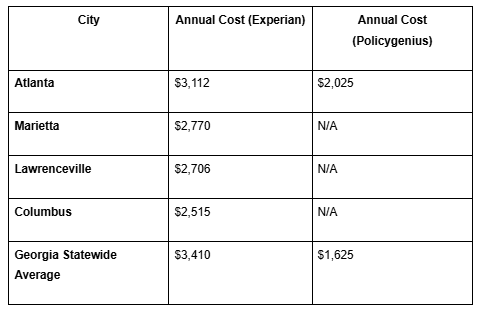

The first step in understanding Atlanta’s auto insurance market is to recognize its unique position within the state. Data consistently shows that living in the city itself can result in a significant premium—a phenomenon often referred to as the “Atlanta Tax.” For a full coverage policy, the average annual cost in Atlanta is approximately $2,025, which is higher than the Georgia state average of $1,625. This disparity is sometimes more pronounced in other analyses, with some sources citing an average Atlanta premium as high as $3,112 per year compared to a statewide average of $3,410. This difference visually illustrates how a driver’s location can influence their rates, with urban areas typically priced higher than the state average.

The wide discrepancy in reported average costs for Atlanta, which range from $1,391 to $3,112, is not an error in the data. Instead, this variation is a typical characteristic of the insurance market that proves a single, generic average is not a reliable metric for a consumer’s actual premium. The differing averages stem from diverse data methodologies, sample sizes, and the specific driver profiles used in each study, such as age, credit score, and driving history. This highlights the central idea that the only way to know a true rate is to get a personal quote tailored to one’s unique circumstances. Furthermore, the cost of auto insurance is rising across the entire state, with one source reporting a statewide increase of over 21% from 2023 to 2024.

The following table provides a general illustration of this financial disparity.

1.2. The Anatomy of a High-Risk City

Premiums in Atlanta are higher for a combination of reasons that can be traced to the city’s dense, urban environment. The single significant factor is the increased risk of claims, which insurance companies use to determine rates. This is a direct consequence of the city’s rapid population growth, which has not been matched by a corresponding increase in infrastructure, leading to more congested roadways. This continuous loop creates a causal chain of risk: urban population growth leads to increased traffic congestion, which can result in a higher frequency and severity of accidents, culminating in more insurance claims that drive up premiums for every driver in the area.

Beyond the daily traffic grind, Atlanta faces specific local challenges that may escalate risk. Wrong-way crashes, for instance, are not uncommon on major interstates such as I-75, I-85, and I-285. These incidents are particularly devastating because they often involve high-speed, head-on collisions that result in catastrophic injuries or even death. The resulting insurance claims are often complex, involving multiple vehicles, disputes over liability, and damages that far exceed the at-fault driver’s policy limits. These high-cost claims contribute to the overall premium increases for the entire market. In addition to accidents, higher rates of auto theft and vandalism in certain zip codes may add another layer of risk, forcing insurers to adjust premiums to cover potential losses from these incidents.

Furthermore, national economic trends are amplified in a major metropolitan area like Atlanta. Inflation has a direct impact on the auto repair industry, making it more expensive for insurers to cover claims. The increasing sophistication of modern vehicles, which are equipped with expensive sensors and computers, also contributes to higher repair costs, as these parts must be replaced even after minor collisions. All these factors can create a risk environment that forces insurance companies to charge higher rates to remain solvent, making the search for affordable coverage a critical financial exercise for Atlanta drivers.

Section 2: Decoding Your Personal Rate: The Factors You Control

While the overall market conditions in Atlanta influence premiums, a driver’s personal rate is ultimately determined by a combination of individual factors. Understanding these elements is the key to identifying possible opportunities for savings.

2.1. Your Driving Record’s Financial Impact

An individual’s driving history is one of the significant predictors of future risk for an insurer. A clean driving record is a primary factor in securing lower rates. Conversely, accidents and violations can have a clear and quantifiable financial impact on premiums. For example, a single speeding ticket may increase annual rates by over 25% for a driver with no prior record. More serious offenses, such as a DUI, can have a substantial effect, potentially raising premiums from an average of $1,480 to well over $2,800 annually, depending on the insurance company.

The impact of violations is not always a simple one-to-one calculation. Data from insurers suggests that they view repeated incidents as a strong risk factor. A driver with three or more violations or incidents, such as accidents or claims, may face an exponential rise in their premiums, with some data showing annual costs exceeding $4,000 for those with multiple violations. This is because insurance carriers utilize past behavior to predict future risk. By explicitly linking a clean driving record to a possible financial reward, insurers give drivers a tangible incentive to operate their vehicles safely.

2.2. The Power of Personal Profile

Beyond the driving record, a driver’s personal profile plays a significant role in determining their rate. Age is a major factor, with rates for young drivers in Georgia being significantly higher than for older drivers due to statistical data showing they are more likely to be involved in accidents. For instance, a 16-year-old driver may pay an average of over $6,200 annually, while a driver in their 50s might pay just over $1,100. Rates typically drop significantly after age 20 and continue to decline until a driver reaches their mid-70s, at which point they begin to gradually increase again. Gender also plays a role, with statistics indicating that women are less likely to be involved in serious accidents than men, which often results in lower premiums.

One of the overlooked financial levers is the credit-based insurance score. In Georgia, this score is a key determinant of rates, with drivers who have bad credit typically paying more than double the premium of those with good credit. Insurers use this score to predict the likelihood of future claims. A driver’s credit score is not a static number; it can be improved over time by paying bills on time, limiting debt, and reviewing credit reports for errors. This long-term strategy can be a valuable tool for reducing premiums.

2.3. Policy Optimization: Coverage, Limits, and Deductibles

While a driver’s profile and history are fixed in the short term, their policy can be strategically optimized to reduce costs. One of the direct ways to lower a premium is by raising the deductible. A deductible is the amount a driver agrees to pay out of pocket before their insurance coverage kicks in for a covered loss. Raising this amount lowers the insurer’s financial exposure, which they pass on to the policyholder in the form of a lower monthly premium. This is a strategic financial trade-off: a lower premium is gained in exchange for a higher out-of-pocket cost in the event of an accident. It is important to only raise a deductible to an amount that a driver can comfortably afford.

Another effective strategy is to adjust coverage levels, particularly on older vehicles. Georgia is an “at-fault” state, which means the driver responsible for an accident is also financially responsible for all resulting property damage and bodily injury. Georgia law requires minimum liability limits of $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $25,000 for property damage per accident. However, these minimums may be insufficient to cover the costs of a serious accident, potentially leaving a driver’s personal assets vulnerable to a lawsuit. For an older, paid-off car, a driver might consider dropping optional comprehensive and collision coverage, as the potential payout in the event of a total loss may not be worth the ongoing cost of the premium.

Section 3: Your Action Plan to Find Cheap Insurance Today

The Power of Comparison Shopping

One of the most effective ways to find cheap car insurance in Atlanta is to compare quotes from multiple companies. Insurance rates can vary significantly between providers, as each company uses a different risk model and offers a unique range of discounts. What one company considers a high-risk factor, another may view as a minor infraction. By shopping around and getting quotes from both local Atlanta insurers and national companies, a driver can potentially uncover the most suitable rates for their specific situation.

Unlocking Every Available Discount

Discounts are a valuable tool for saving money, yet they are often overlooked. Rather than seeing them as a simple checklist, drivers should consider discounts as a strategy for compounding savings. Most insurance companies offer a range of discounts, but it is often up to the policyholder to inquire about them.

Common, stackable discounts include:

- Multi-Policy Discount: Insuring both a car and a home or rental property with the same company can lead to potential savings, sometimes reaching 25% on both policies. This is often offered as a multi-policy bundle.

- Good Driver Discount: Maintaining a clean driving record without accidents or violations for a certain period may qualify a driver for lower rates over time.

- Good Student Discount: Full-time students under a certain age who maintain strong grades may be eligible for a discount of up to 2%.

- Telematics (Usage-Based Insurance): Many insurers offer programs that track driving habits, such as braking and speed, through a smartphone app or a device installed in the car. Safe drivers may earn a discount based on this data.

- Paid in Full/Automatic Payments: Paying for the entire policy term upfront can save a driver up to 12%, while setting up automatic payments from a bank account may save up to 2%.

- Vehicle Safety Features: Cars equipped with anti-theft devices, anti-lock brakes, or other safety features might qualify for discounts.

Section 4: A Granular Look at the Atlanta Market

4.1. The ZIP Code Lottery: Rates by Neighborhood

The zip code of a driver’s residence is a crucial factor in premium calculations, as it reflects the local risk of the area. Insurers analyze data on local accident rates, traffic congestion, and auto theft statistics to determine the risk level of each neighborhood. A driver in a zip code with a higher number of incidents may face a higher premium than a driver in a less risky area, even within the same city. The data confirms this, with a wide range of average costs even within Atlanta, from $1,744 in the 30327 zip code to $1,915 in the 30345 zip code. This variation underscores the need to get a personalized quote, as a driver’s exact location can significantly impact their rate.

4.2. Tailored Savings for Every Driver Profile

For higher-risk drivers, finding affordable insurance can be a particularly frustrating challenge. However, this analysis shows that there are specific companies that specialize in providing coverage for these profiles. By understanding which insurers are more favorable to certain risk factors, a driver with a less-than-perfect record may find a clearer path to a lower premium.

Section 5: Frequently Asked Questions (FAQs)

- What are the minimum car insurance requirements in Georgia?

Georgia state law requires all drivers to carry a minimum amount of liability coverage. This coverage must meet the following minimum limits: $25,000 for bodily injury liability per person, $50,000 for bodily injury liability per accident, and $25,000 for property damage liability per accident. While this is the legal minimum, it is often advisable to choose higher coverage limits to protect against significant accidents. -

Is Georgia a no-fault state?

No, Georgia is an at-fault state. This means that the driver who is determined to be at fault for an accident is financially responsible for the bodily injuries and property damage of all other parties involved.

-

How do I check my insurance status in Georgia?

A driver’s insurance company is required to send proof of coverage to the Georgia motor vehicle database electronically. To verify if their insurance information is correct and active, a driver can check their insurance status online through the state’s motor vehicle database.

-

What should a driver do immediately after a car accident in Atlanta?

In the event of an accident, a driver should first ensure everyone’s safety and move their vehicle to the side of the road if possible. Then, exchange contact information, insurance details, and license plate numbers with all other parties involved. Taking photos of the accident scene, vehicle damage, and any relevant road signs is also a helpful step for documenting the incident. Drivers should contact the police to report the accident and gather the names of any witnesses.

-

How can a driver know if they have enough coverage?

A driver can determine if their coverage is sufficient by reviewing their policy documents and considering their personal financial situation. While the state minimums may suffice for some, it is advisable to choose liability limits that are high enough to cover the value of a driver’s assets.

Summary: Your Path to Affordable Car Insurance in Atlanta

Finding affordable car insurance in Atlanta requires a proactive, informed approach that goes beyond simply accepting the first quote. While the city’s unique blend of traffic, population density, and high-cost claims leads to premiums higher than average, this challenge is not insurmountable. The key is to recognize that a driver’s rate is a function of their unique profile, not a generic average. By strategically optimizing a policy, leveraging available discounts, and understanding which insurers are most competitive for their specific circumstances, a driver can potentially reduce their costs. The path to savings is one of diligence and smart decision-making.

Disclaimer: This article is for informational purposes only and should not be considered as professional financial or legal advice. Insurance premiums can vary greatly based on individual circumstances, and it is important to consult with an insurance professional to obtain accurate and personalized quotes. The rates mentioned are averages, and individual results may differ. Always review and compare insurance policies before making a decision.